India’s Rise as the Next Silicon Valley

How Deep Tech, AI, and Clean Tech Unicorns Are Building the Future

“The next unicorns won’t sell ads—they’ll build satellites and clean cities.”

Introduction: The New Growth Engine

India’s ascent to the global startup pantheon is no longer a bet—it’s a reality. With over 159,000 DPIIT-recognized startups, India now ranks as the third-largest startup ecosystem globally, trailing only the U.S. and China. From fintech and gig-tech to deep tech and cleantech, the country is crafting a unique innovation blueprint that is drawing global attention.

Funding Momentum & Unicorn Surge

Even with a cooling global funding climate, Indian ventures have pulled in $5.7 billion across 470 deals in H1 2025, producing five new unicorns across sectors from agri-tech to ISO‑certified EV infrastructure. Across 2024, total startup funding reached $7.4 billion, growing 23% YoY, with a notable shift toward mature, revenue‑driven startups rather than speculative early-stage bets.

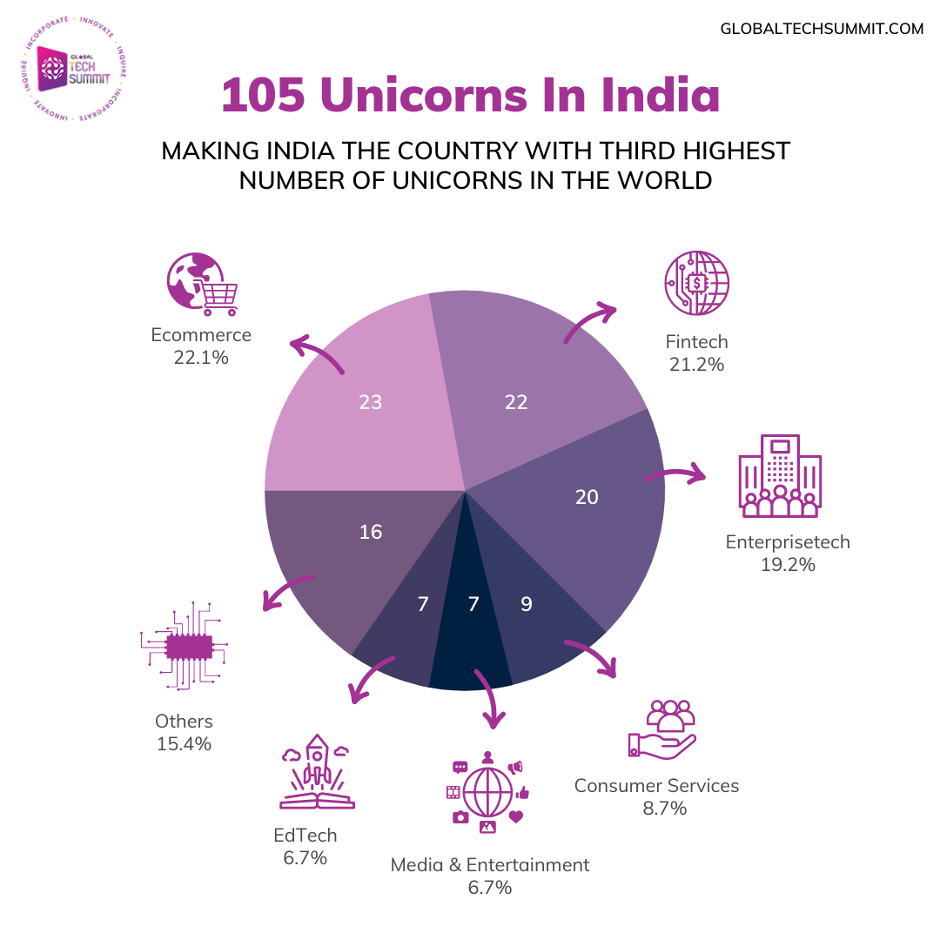

As of mid‑2025, India boasts 110 unicorns with a collective valuation nearing $600–700 billion. Flagship names like Netradyne, India’s first autonomous fleet‑safety AI unicorn, and Ather Energy, the IPO‑bound EV pioneer, exemplify the ecosystem’s rising stars.

Deep Tech & AI: India’s Innovation Frontier

Deep-tech startups—covering AI, robotics, biotech, semiconductors, robotics, and space tech—are rapidly scaling. There are around 4,000 deep-tech companies, expected to reach 10,000 by 2030. In 2024 alone, they raised $1.6 billion, up 78% YoY.

Leading innovators include Pixxel, which is building a constellation of hyperspectral imaging satellites for agriculture and climate monitoring, and Neysa, offering cloud GPU infrastructure and MLOps platforms for generative AI applications.

Government & Institutional Backing

The federal government’s renewed startup agenda has added ₹10,000 crore (~$1.25 billion) for deep-tech funding via SIDBI’s Fund-of-Funds, along with tax incentives, compliance relief, and incubation support under Startup India and the National Deep Tech Startup Policy .

Institutes like IISER Bhopal, IIT Bombay, and IIT Madras are strengthening incubators and innovation hubs for sustainable tech and AI research, creating a formal bridge between academia and the startup ecosystem.

Flagship Unicorn Case Studies

Netradyne

Bengaluru-based Netradyne became India’s first fleet-tech unicorn in 2025, after raising $90 million in a Series D led by Point72. Its AI‑enabled dashcams serve 3000+ global clients, analyzing 18 billion miles of driving data to improve safety and operations across seven countries.

Ather Energy

The two‑wheeler EV pioneer, backed by NIIF, hit unicorn valuation (~$1.3 billion) in 2024 and is heading toward an IPO milestone in late 2025. Ather’s success reflects both domestic EV demand and cleantech investment potential.

Neysa

This AI‑cloud infrastructure startup raised $50 million in under two years to position itself as a local alternative to global GenAI hyperscalers, empowered by high‑performance GPU platforms and enterprise security tools.

Challenges & Cautions Ahead

Rapid growth comes with risks. As Shark Tank India judge Anupam Mittal warns, technology must be balanced with job creation and inclusion; simply chasing deep tech could leave critical social needs unmet.

Meanwhile, a tidal wave of new developers faces challenges: over five million coders are expected to reach global parity by 2027—but automated AI tools may disrupt traditional software roles, stressing the need for reskilling and infrastructure investment.

The Road Ahead: Why It Matters Globally

India is poised to lead the emerging vertical AI market, projected to reach $47 billion by 2030, in domains like healthcare, agriculture, financial services, and manufacturing. As U.S.-China decoupling accelerates, India is increasingly central to global tech strategies and capital flows. Funds like Bat VC are raising $100 million to back early-stage India–U.S. AI firms, signaling growing cross-border collaboration and returns potential.

- India’s Startup Rise

Years: 2016 → 2025

- 2016: 4,000 startups

- 2020: 50,000

- 2022: 80,000

- 2025: 159,000+ startups

- Sectors Driving the Boom

- AI & Deep Tech – 28%

- Fintech – 21%

- CleanTech & EV – 17%

- HealthTech – 14%

- Agritech & RuralTech – 10%

- Others – 10%

- Unicorn Map: Where They’re Built

- Bengaluru: 47%

- Mumbai: 21%

- Delhi-NCR: 15%

- Hyderabad, Chennai, Pune, Others: 17%

Conclusion: The Case for India 2.0

India’s burgeoning startup ecosystem is no mere fringe movement—it’s a structurally driven ascent led by deep tech, policy alignment, and growing global capital. The narrative has shifted: India is not just following Silicon Valley—it’s building its own, tailored to emerging global demands.

As the world watches vertical AI, climate tech, and mobility innovation take shape in India, the question is no longer if India will dominate the next wave—it’s when.

“India isn’t just competing—it’s defining the global tech future.”

— Accel India, 2025

“Deep tech will be India’s moonshot moment. We’re almost there.”

— Rajan Anandan, Peak XV Partners